Marine Engines Market: Global Trends, Growth Drivers, and Future Outlook (2024–2030)

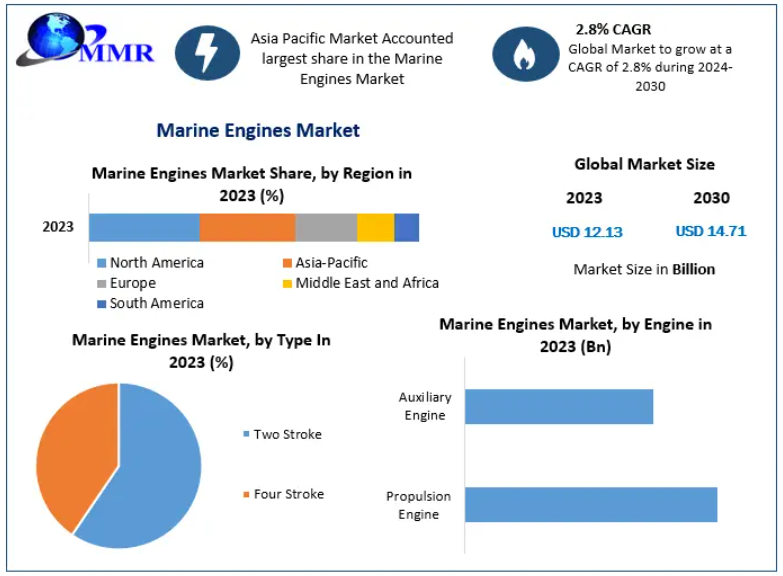

The Global Marine Engines Market, valued at USD 12.13 billion in 2023, is projected to reach USD 14.71 billion by 2030, expanding at a CAGR of 2.8% during the forecast period. The rising volume of international maritime trade, growth of the global shipbuilding industry, and technological advancements in marine propulsion systems are shaping the positive trajectory of the market.

Market Overview

Marine engines are critical propulsion systems used across all types of vessels—ranging from small boats navigating coastal waters to large cargo ships crossing international sea routes. Historically dominated by reciprocating steam engines, the marine propulsion landscape has evolved significantly, with steam turbines, internal combustion engines, electric motors, and advanced hybrid systems becoming key technologies.

Marine engines function by converting thermal energy generated from fuel combustion into mechanical energy. Both 2-stroke and 4-stroke engines are used extensively depending on vessel type and operational requirements. These engines remain indispensable for global logistics, offshore operations, passenger transport, and naval applications.

To know the most attractive segments, click here for a free sample of the report: https://www.maximizemarketresearch.com/request-sample/11261/

Scope of the Report

This market analysis provides maritime stakeholders with a deep understanding of:

- Historical and current market developments

- Market structure and segmentation

- Competitive landscape and benchmarking

- Technological, regulatory, and macroeconomic influences

- Forecast trends through 2030

The report integrates PORTER’s Five Forces, PESTEL analysis, and microeconomic assessments, enabling strategic decision-making for investors, manufacturers, and shipping companies. The research employs a Bottom-Up methodology, supported by extensive primary and secondary data.

Market Dynamics

1. Rising International Marine Freight Transportation is Driving Market Growth

Marine transport remains the backbone of global trade. According to UNCTAD, over 80% of international goods by volume are transported via sea routes. This dominance is attributed to cost-effectiveness, capacity to transport large quantities, and global accessibility.

Post-pandemic recovery has increased vessel demand due to:

- Restocking and inventory buildup

- Surge in consumer demand

- Shortage of containers and shipping capacity

- Renewed investments in fleet expansions and retrofitting

These factors are pushing shipowners to purchase new vessels or upgrade older ones—directly boosting the demand for marine engines.

2. Growth of E-Commerce Creating New Maritime Trade Opportunities

The pandemic accelerated e-commerce adoption by nearly five years, driving rapid growth in digital trade. Massive increases in online orders have intensified pressure on global logistics, leading to:

- Port congestion

- Shortages of containers and cargo vessels

- Rising storage and distribution needs

This trend is expanding opportunities for:

- New cargo ships

- Higher engine installations

- Digitized marine operations

- Port logistics and warehousing

As maritime transport remains the most cost-efficient long-distance shipping method, the rise of e-commerce will continue driving marine engine demand.

3. Environmental Regulations Pose Challenges but Accelerate Innovation

The shipping industry faces strict global emission regulations, especially from the International Maritime Organization (IMO). Decarbonization goals require:

- Cleaner fuels (LNG, methanol, biofuels, ammonia, hydrogen)

- Low-sulfur fuel alternatives

- Advanced emissions-control technologies

- Fuel-flexible marine engines

Compliance costs are substantial, prompting some shipowners to delay new vessel orders. However, these regulations are also driving innovation in green engines, hybrid propulsion, and digital fuel-optimization technologies.

Market Segment Analysis

By Type

Two-Stroke Engines – Largest Segment (2023)

Two-stroke engines dominate due to:

- High power-to-weight ratio

- Ability to run on low-grade fuels

- Higher efficiency for long voyages

- Use in large ocean-going cargo vessels

Global maritime trade growth will further strengthen demand for two-stroke marine engines.

By Fuel Type

Heavy Fuel Oil (HFO) Leads the Market

Despite rising environmental regulations, HFO remains widely used due to its availability and cost advantage. However, regulatory pressures are shifting demand toward:

- Marine diesel oil (MDO)

- Marine gas oil (MGO)

- Low-sulfur fuels

- Alternative clean fuels

The marine diesel oil segment is expected to grow as refiners prioritize low-sulfur marine fuel blends.

By Ship Type

Bulk Carriers – Leading Segment

Bulk carriers transport major raw materials such as:

- Iron ore

- Coal

- Grains

- Bauxite

- Fertilizers

As global demand for raw materials increases and freight rates stabilize, new bulk carrier orders are rising—fueling marine engine installations.

To know the most attractive segments, click here for a free sample of the report: https://www.maximizemarketresearch.com/request-sample/11261/

Regional Insights

Asia Pacific – Market Leader

Asia Pacific accounts for the largest market share due to:

- Strong shipbuilding industries in China, South Korea, and Japan

- Expanding maritime trade

- Low labor costs and manufacturing advantages

- Growing exports of electronics, machinery, and industrial goods

China leads in bulk carrier and cargo ship production, while Korea dominates LNG tankers and container ship manufacturing.

Europe – Second Largest Market

Europe is home to:

- The world’s largest commercial fleet

- Major cruise ship and luxury yacht manufacturers

- Strong regulatory frameworks supporting green marine technologies

The EU shipping industry contributes €147 billion to regional GDP, enhancing demand for advanced, efficient engines.

North America – Growing Market

North America is experiencing strong growth supported by:

- Rising offshore exploration

- Seaborne trade expansion

- Technological advancements in marine engines

- Strong demand for commercial and recreational vessels

Consolidation among industry players and focus on high-performance engines will further drive growth.

Key Market Players

Major companies operating in the Marine Engines Market include:

- GM Powertrain

- Caterpillar Inc.

- Cummins Engines

- Wärtsilä Corporation

- Rolls-Royce

- MAN Diesel & Turbo SE

- Mitsubishi Heavy Industries

- Hyundai Heavy Industries

- Scania

- YANMAR Co. Ltd.

- Daihatsu Diesel Mfg. Co. Ltd.

- Niigata Power Systems

- Fairbanks Morse Engine

- Masson-Marine

- General Electric Company

- Mercury Marine

- Sumitomo Heavy Industries

- Brunswick Corporation

- AB Volvo

- John Deere

- Dresser-Rand Group

- Deutz AG

- STX

These companies focus on innovations in dual-fuel engines, hybrid propulsion, low-emission technologies, and digital engine monitoring systems.

Future Outlook

Between 2024 and 2030, the Marine Engines Market will evolve with advancements in:

- Alternative fuels: LNG, methanol, ammonia, hydrogen

- Hybrid and electric propulsion

- Fuel-efficient two-stroke engines

- Smart engine monitoring and automation systems

- Eco-friendly ship designs

Decarbonization will remain a defining theme, pushing manufacturers to innovate while maintaining high performance and durability standards.